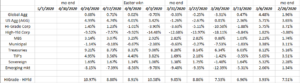

This is a spreadsheet kept on Bloomberg bond market data, which i find very helpful (the Bloomberg data, not the spreadsheet). The data is thrown up once a week to keep an eye on asset classes that don’t really get much attention from the mainstream financial media.

The spreadsheet shows the pain in the various bond market categories before and through the pandemic worries and then the start of the Fed stimulus.

HYG, iShares High-yield ETF is down 9.71% YTD, and you can’t help but wonder how much is due to the Energy sector, with Diamond Offshore filing for bankruptcy this weekend.

HYG’s weighting in Energy per the iShares ETF website, is 8.5%.

What may me more interesting to readers is that iShares started an “ex gas and oil” ETF with the ticker HYXE. The HYXE was down 7.09% as of April 24th, 2020.

As of last Friday, investment grade corporates total return vs high yield total return was at its highest spread of the pandemic.

The drop in high-grade credit during the week of March 23rd was truly frightening: between March 9th and March 19th, the LQD (investment-grade ETF) dropped from $133 to $104.95.

Summary / conclusion: Using Morningstar data, the above spreadsheet was started to keep a weekly eye on bond market asset classes, since monthly index data is too infrequent. Tracking fixed-income sector ETF’s (like the MBB or Mortgage-backed ETF) is helpful too.

The point of the post is that while high-yield struggled last week, including muni high-yield, the asset class remains relatively attractive from a “current yield” and an “expected total return” perspective.

The Fed stimulus and liquidity expansions, such as the liquidity lines as well as buying select high-yield credits for the Fed balance sheet should help support the asset class.

Energy, retail, mall CMBS, and airline credits are all sectors under severe stress.

The Energy sector is likely to see the biggest rash of immediate bankruptcies due to the drop in crude oil, but all of the above will likely see filings.

The mainstream financial media doesn’t offer give the credit markets the attention they deserve. A Constellium high-yield credit yielding 8.5% that no one’s ever heard of isn’t nearly as interesting as Amazon or Zoom, but the asset class is very important to healthy functioning of the capital markets.

The difference in total return between the HYG and the HYXE is one tell that high-yield in general remains cheaper relative to high-grade and higher-rated credits.

Take this opinion and all opinions with substantial skepticism. The markets change quickly and the data might not be updated with any frequency or at all.

Thanks for reading.