Normally, the “Style Box Update” is done mid-quarter and then the last day of the quarter, but Tuesday might be busy.

Growth is still hammering Value, and by a wide, wide, margin. No doubt Energy and now the Financial sector have dragged the “value” style through the gutter. Clients over overweight Financials, but haven’t owned any Energy since 2017.

Across every market-cap, Growth is outperforming Value by at least 1,000 bp’s YTD in 2020, in both a “good” market (positive SP 500 return) and a “bad” market.

Small and Value really haven’t generated alpha since 2016.

Does this mean it’s time to reallocate ? Consider this blog post when thinking about relative performance.

———

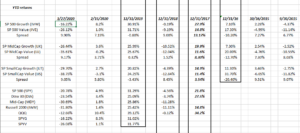

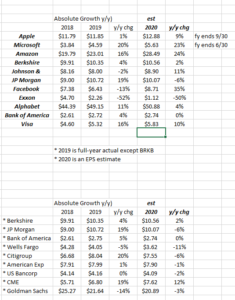

Updating the “Top 10” Stocks in the SP 500 this weekend, is harder than it looks. Exxon and Bank of America have now fallen out of the “Top 10” market cap weights in the SP 500.

What is being shown in this table is the Top 10 SP 500 weights (Procter & Gamble is now #10 and not shown) and their current “estimated” 2020 EPS growth as of this weekend. (EPS Estimate source: IBES by Refinitiv.)

The “average” EPS growth for full-year 2020 is still 6%. While Amazon is considered Consumer Discretionary, the top 4 names in the SP 500 this weekend are Microsoft, Apple, Amazon and Facebook.

- Top 3 names comprise 14% of the SP 500 by market cap

- Top 5 names comprise 17.5% of the SP 500 by market cap

- Top 10 names comprise 26% of the SP 500 by market cap (versus 23.6% as of 2/15/20)

The second part of the table above is the top 9 Financial names in the SP 500, only two of which remain in the Top 10, and those are Berkshire and JP Morgan. Financials as a % of the SP 500 have fallen from 15% of the SP 500 to just 11% as of this weekend.

The “average” expected earnings growth for the top 9 names in the Financial sector is -2%, per the above table. CME is expecting the best EPS growth in 2020, probably thanks to the surge in volume in March ’20.

Clients are overweight Financials in their accounts in a nod to “Value” investing, and those positions are JP Morgan (JPM), Charles Schwab (SCHW) and Chicago Merc (CME).

This post Friday night highlighted the drop in the Financial weighting within the SP 500.

———————–

Great article by CNBC’s Michael Santoli in the 20% YTD drop in the standard 60% / 40% asset allocation portfolio, and what it potentially portends for the US stock market. Michael Batnick at Ritholtz Wealth does great research work.

———————-

Lots of folks calling the SP 500 bottom:

- Paul Tudor Jones

- Leon Cooperman

- Larry Fink

Gary Morrow, our favorite technician thought the December ’18 low at 2,350 and the lows early last week, would hold.

Ryan Detrick wonders if there aren’t too many rushing in here trying to call the bottom.

The only thing I’ve told clients is to wait for the retest and then we’ll see.

——————–

Still fascinated by the notion that a 20% SP 500 correction is a bear market. Who anointed this number ? Did it get traction because it allows mainstream and financial media to raise the decibel level on market noise ? If I sold all my taxable accounts out and went to 100% cash in a market that corrected 20% and then ended the year (even just) somewhat better than that, and hit clients with a capital gains tax bill, there would be no assets at all to manage.

——————–

Many thanks to Josh Brown at Rithottz Wealth for trying to stay positive throughout this ordeal. Josh has steadfastly tried to be balanced about the news flow and market impact for several weeks now on CNBC, despite the fact the mainstream financial media lives for the drama. I worry that this is going to get politicized shortly and it’s started in Illinois as Governor Pritzker has started blaming President Trump. Even as the virus data will eventually improve with testing and the communication to the general public about the virus, the Presidential election will drive this whole thing right into the gutter.

———————

Two major sector potholes that have been avoided for clients the last few years are Energy and Retail. No Energy has been owned at all, although some smaller long positions have been taken in retail over the last 5 – 8 years, like a JC Penney (JCP), when Marvin Ellison was CEO, Bed Bath (BBBY) when it was trading at 1x cash-flow, and UnderArmour (UAA) which was probably clients largest position and held the longest. UAA had to be sold when it disclosed the Justice Department investigation at the same time it disclosed the SEC accounting investigation (and the SEC investigation should have been disclosed much earlier). Justice Dept is a criminal matter and that’s an automatic sell. Clients lost money on JCP and BBBY, but it was a mixed P/L on UAA. The new CEO at Bed Bath is likely guilty of bad timing only: what a horrid time to try to turnaround a retail business. I’m surprised they don’t go private.

Thanks for reading. Remember this is all just one opinion, and I always try to update for readers, but don’t always get around to it.