Rick Rieder, Blackrock’s CIO, held his monthly call with investors on Monday, April 7th at 7 am central time. Usually this call is held the first Thursday of the month, but with the market action last week, Rick pushed it off until Monday, to give it a few more days.

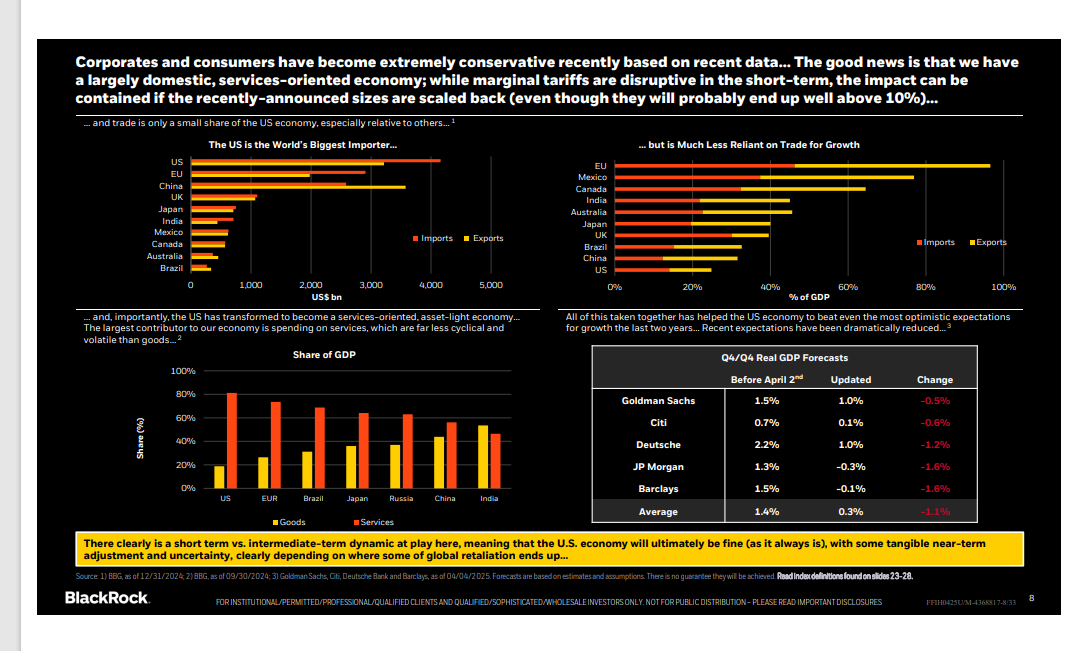

This table was page 8 of Blackrock’s slide packet, and if readers click on the image and enlarge it, while the two slides at the top of the page show that the US is the world’s largest importer in the world (not a surprise, probably due in no small part to the US being the largest economy in the world with annual GDP growth of around $30 trillion per year), the slide in the upper-right hand corner shows the US economy is much less reliant on trade for growth. Of the 9 countries listed, the US is the least of the countries or trade blocs like the EU, that is reliant on imports for growth.

China is just above the US in the “trade reliance for growth” slide in the upper-right hand corner.

The fact is this surprised me, and not a little.

The current Administration is now engaged in a game of trade chicken versus China, and with the leverage still in America’s favor (given the above chart), and ultimately you would think the US should prevail. The one challenge is that Xi Jinping, can simply tell the Chinese people, “look, you’re going to have to endure this however longs it takes”. Xi doesn’t have to run for re-election.

Way back in 1998, around the time of the Russian debt default, John Meriweather, formerly of Salomon Brothers, founded LongTerm Capital Management, ran into trouble as the Street started taking opposite positions in his hedge fund’s Russian credits, and it ultimately caused Alan Greenspan to ask the major commercial and investment banks at the time to bail out LongTerm Capital. (This was the first real whiff of “systemic risk” that would ultimately rear it’s ugly head in 2007 and 2008. )

The point is, at least according to the book, “When Genius Failed” by Roger Lowenstein, and numerous articles that followed the collapse, Greenspan was getting quite concerned about the corporate bond spreads, and their relationship to Treasuries (and this was about more than just spread-widening I believe), and Greenspan chose to lower the fed funds rate in September, 1998, while the actual market – meaning the SP 500 and the Nasdaq – didn’t bottom until October, 1998.

Greenspan ultimately reduced the fed funds rate from 5.25% in September ’98 to 4.50% into ’99, and it lit the stock market like a Roman candle. (This was in the period from 1995 to 1999 when the SP 500’s “average, annual return” was 28.5% per year. )

So, what’s the point ?

The point of relating 1998 LongTerm Capital memory is that what is happening within Treasuries, might motivate the Fed and FOMC and Powell, to move sooner rather than later, also supported by the very favorable drop in the March, Core CPI and overall CPI, and the PPI data this week.

The “inflation expectations” component of this morning’s U of Michigan Consumer Sentiment Report was not as favorable as the March CPI data, and that’s got everybody’s attention. The year-ahead inflation expectations metric within the U of M report shot higher to 6.7% from 5%.

The “basis trade” might have a liquidity component to it, and the FOMC will not tolerate too much of that.

High-yield credit spreads jumped to an average of +437 (per the Bespoke data) as of this morning, from last week’s +350 over the equivalent Treasury. That’s the highest spread seen since the +415 on 11/3/2023.

The spread-widening may not solely be the expectation of a weaker economy, but could also be a function of the Treasury volatility.

Again, the point being the FOMC and Jay Powell may be easing sooner than was originally expected.

Summary / conclusion: Take this for what it’s worth. Some of the “basis trade” comments and the leverage therein with the basis trade, resulted in me thinking about LongTerm Capital and that period in 1998.

The SP 500 and Nasdaq peaked in late July ’98 and then investors watched the market really trade down hard in August ’98 and then the first half of September ’98, and while I work alone, and don’t have fellow portfolio managers or traders to yap with, there was an element in the financial media and the research at during late July, early August ’98 of “what’s driving this ?” until David Faber broke the story about LongTerm Capital before Greenspan cut the fed funds rate. (I believe Faber broke the story before the first fed funds rate cut, but that could be wrong.)

If you think the markets were volatile around tariffs, the Nasdaq corrected 35% from it’s late July ’98 high to it’s early October ’98 low) before rocketing higher in the Q4 ’98.

Illiquidity isn’t good for the bond markets. Rick Santelli, the CNBC economics reporter that reports from the floor of Chicago’s CME, talked a little about the “basis trade” and illiquidity this week in one of his reports and he didn’t yet think it was critical.

The Fed and some of the Fed Governor’s like Austin Goolsbee have said that the Fed’s monetary policy remains well above the neutral rate. The good March inflation data this week is a plus. Inflation expectations were not.

Once again, Monday morning and any news over the weekend, will drive another set of opinions.

None of this constitutes a recommendation or advice. Past performance is no guarantee of future results. Investing can or does involve the loss of principal even over short periods of time. None of the information above may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.