No sooner did we have one solid week for the stock and bond markets as the seasonally-favorable part of the calendar began, when the gloom-and-doomers come out of the woodwork, and start yelling “the sky is falling” when it comes to SP 500 earnings.

Don’t buy into the disaster-is-nigh crowd just yet. Here’s a couple of aspects to SP 500 earnings to consider:

1.) Full-year 2023 SP 500 earnings growth is expected to be 2% – 3%, versus 6% actual growth in 2022, and yet the SPY was up 14.94% as of 11/3/23, in what seems like a difficult year. The knee-jerk reaction is to always trim SP 500 EPS expectations, but here’s the kicker: in 2019 SP 500 EPS growth was 0% and the SP 500 returned 31.8%, thanks to Jay Powell and the FOMC cutting interest rates.

2.) In Q4 ’23 and early 2024, the SP 500 faces weak compares vs the Q4 ’22 and early 2023 actual SP 500 earnings results. Here’s a look at the numbers:

- Q4 ’22 y.y EPS gro: -3.2% EPS gro, +5.8% rev gro;

- Q1 ’23 y.y EPS gro: +1% EPS gro, +3.6% rev gro;

- Q2 ’23 y.y EPS gro: -2.8% EPS gro; +0.5% rev gro;

The 3rd quarter of 2023, being reported currently is the strongest quarter of SP 500 EPS growth since Q2 ’22.

3.) The final aspect to SP 500 estimates is that not ALL of the estimates put up are bottom-up SP 500 estimates run through models. John Butters or Michael Thompson, both of whom were at Refinitiv (before it was Refinitiv) told me that half the full-year SP 500 EPS estimates are thrown up by strategists, which can be somewhat – how shall we say – less rigorous, than a bottom-up earnings model. If Mike Wilson of Morgan Stanley would have thrown up a full-year 2022 or 2023 SP 500 estimate (or estimates) where do readers think it would have landed relative to consensus ? Not to pick on Mike. but to make the point about all the erroneous recession calls of the last 18 months, and what that does to the “mean” estimate.

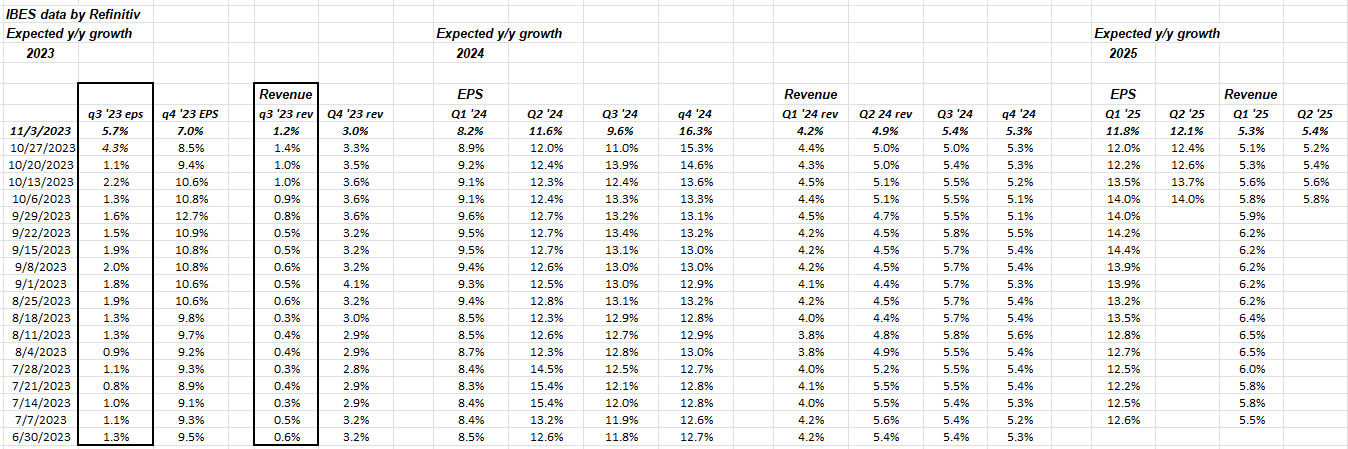

Here’s a table I like to show on occasion: look at the reduction (by quarter) in the last week:

The two columns highlighted are Q3 ’23 EPS and revenue growth. Note the cuts to forward EPS and revenue growth this week.

Remember, stock market return has more to do with liquidity than SP 500 earnings growth.

What’s even more interesting is that SP 500 EPS is expected to grow in 2024 11% as of this weekend. That’s down from 12% a week or two ago. If the Fed does reduce rates in 2024, investors could be facing a double-barreled tail wind of decent SP 500 earnings growth and easier monetary policy.

The point for readers is to use caution around SP 500 earnings that are too far in either direction in terms of optimism or pessimism. I wouldn’t be surprised to see the “expected 11% 2024 SP 500 EPS growth get trimmed over the next 7 weeks, possibly to mid-single-digit expected growth.

The “upside surprise” or beat rate to SP 500 EPS in this Q3 ’23 is still at 7% even with 80% of the SP 500 having already reported. The headlines, the FOMC, the Fed’s statements, the constant negativity in the news media has driven earnings expectations and analyst estimates far too low, as evidenced by the “beat rate” of SP 500 earnings being +6.8%, +7.9% and +7.0% the last three quarters.

Q4 ’23 is facing very easy comp’s per the above numbers. It should be another healthy quarter for the SP 500 reports.

Summary / conclusion: Take all of the above with substantial skepticism as it represents just one opinion, and it neither advice nor a recommendation. Past performance is no guarantee of future results. Investors are entering into the seasonally-strongest part of the calendar for positive stock returns, and SP 500 earnings were/are for Q3 ’23 – once again – healthy. Certainly not blow-outs for most but the +5.7% EPS growth for Q3 ’23 as of Friday, 11/3/23, is far healthier than the +1.6% expected on for the quarter on 9/30/23.

If you are wondering what to watch, along with SP 500 earnings, for a US economy that might decelerate too quickly, watch corporate high yield credit or “junk” bonds. Corporate high yield had a good week last week – the HYG alone returned 3.18% last week. One metric tracked each week, is the return on high yield credit (HYG) versus the return on investment-grade credit and high yield is still +600 bp’s better YTD as of 11/3/23.

If “duration” starts to catch up to credit, this spread should narrow, and if the US economy does start to decelerate faster than many expect, it’s likely to start to show up in credit spreads first.

Rightly or wrongly, I’ve always felt that credit spreads were the early-warning detection system for US economic problems.

Thanks for reading.