In the weekly SP 500 Earnings update this weekend, some thoughts were given on the Technology sector’s earnings, forward growth estimates, and the influence Apple has on the sector.

Readers should quickly look at this blog post from a few weeks to understand the importance Apple has to both the SP 500 and the Tech sector.

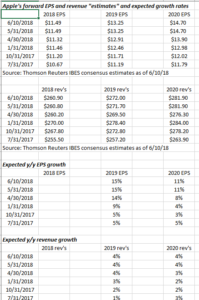

The following EPS and revenue table for Apple was compiled today just to update myself on how Apple’s prospects are being viewed by the Street, after WWDC this past week:

With just 2 quarters left in Apple’s fiscal 2018 (ends 9/30/18), the focus is on 2019 and 2020 EPS and revenue estimates for the technology giant.

The fact is – while EPS growth is looking healthier the last 6 months for fiscal ’19 and ’20 – revenue growth is still expected to be subdued after 2018’s 25% EPS growth and 14% revenue growth respectively.

Studying Apple’s trading history, the last two big iPhone cycles, spanning both 2012 – 2013 and 2015 – 2016 saw sharp selloffs in the stock after a full-year of the new iPhone sales.

Will history repeat itself ? The emergence of the Services business may eliminate that nascent cyclicality. Did Tim Cook pull-off something no Tech giant did in the 1990’s by identifying and nurturing an internal business like Services and the Apple ecosystem, that could eventually sustain forward growth even if Apple’s hardware business falters ?

CNBC ran an article on their blog this weekend stating that the Apple Watch could start to identify or differentiate between Parkinson tremors on its wearers – for me that is the real opportunity for Apple in the next 10 – 15 years, as the combination of “wearables” and the health sector start to combine disciplines to transmit important healthcare information to medical providers.

However, something is happening within Apple’s business model that is resulting in less cash-flow generation versus net income in the last few years, but it may not mean much if these other business – like the Services business, which is a higher margin business – can become a driving force within Apple.

Analysis / Conclusion:

1,The increase in Apple’s forward EPS estimates versus Apple’s revenue estimates likely means the stock buyback is driving a good chunk of the growth – certainly not a negative.

2.) This blog’s articles on Apple’s cash-flow vs net income may also be navel-gazing if the Services business can offset hardware declines, and margin compression in the iPhone business.

3.) After living through the Tech collapse in the early 2000’s and watching the capital markets for 26 years, one painful lesson learned is that nothing grows forever. Frankly I think Tim Cook has done a phenomenal job, essentially trying to identify and nurture new businesses within Apple, particularly the Services business which is an annuity like business, to eventually replace hardware growth.

4.) My own biggest worry around the stock is that the Apple iPhone pricing dynamic has turned technology hardware pricing on its head. It’s very impressive that Apple has been able to drive ASP (average selling price) increases over time in the iPhone. Are the ASP increases sustainable ?

To conclude, while the $1 trillion market cap for Apple just means that Apple has to trade to just over $200 per share, and the stock will probably eventually trade there, a good chunk of Apple has been sold for clients mainly in tax-deferred IRA accounts but kept in taxable accounts given the capital gain.

Too early – probably. Trading at 15(x) forward earnings and 13(x) cash-flow (ex cash) the valuation isn’t unreasonable either.

What is the total size of the US economy (GDP) in dollars – $20 to $22 trillion per Wikipedia ?

Does Apple’s market cap at roughly 5% of the total US economy raise a red flag for sustainability of growth ?

Feel free to give your thoughts.