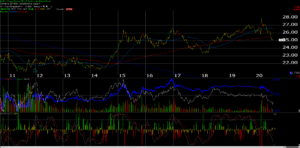

First the weekly chart of the UUP:

Curious as to how the UUP acted in 2016 and then before President Obama was re-elected in 2012, the UUP bottomed almost exactly 4 years ago, during the week of August 23rd, 2020, prior to President Trump’s surprise election, remaining strong through December, 2012. Prior to President Obama’s re-election, the UUP peaked in July, 2012, and weakened throughout the rest of the year. As a caveat, there was a major Greek referendum that July, 2012, where the Greek’s chose austerity, rather than leaving the EU, so that could have had something to do with the change in the direction of the US dollar.

You cant draw any conclusions from two data points but i wanted to show the longer chart.

Emerging Markets:

The emerging markets had a solid July, 2020, up roughly 7% depending on the proxy you use. The rapid slide in the US dollar has helped as – per one source – the correlation between a weak dollar and EM out-performance is 65%.

We’ve written about the EM’s over the years, (here, here and here), and – at present – the asset class represents a “value” or non-momentum offset to our our large-cap tech and growth concentration, which as everyone outside of Siberia knows – continues to generate alpha, and is a substantial part of the SP 500’s return the last 5 years.

In fact to hold EM’s has cost client accounts dearly, but it’s a necessary complement to what is working now.

Reading our previous posts on the subject, it was in Q1 ’16 where the EEM and VWO had their first 10-year negative return in, well. years. That was our initial investment, but it was small 2% – 3% of accounts, but the ETF’s returned 35% – 40% that year. We added more in 2018, and last year, and still today, still taking bite-sized increments of the VWO and OAKIX, (Oakmark International is really developed non-US market play)

Here is an excellent article from Ben Carlson of the Ritzholtz Wealth team published Monday, August 17th, 2020, part of which was taken from the DataTrek Research team’s August 12th post on big-Tech around the globe.

Ben makes a good case for emerging markets in a traditional portfolio.

Here is why I continue to like the asset class and more VWO:

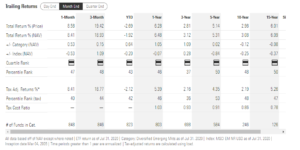

VWO historical return data:

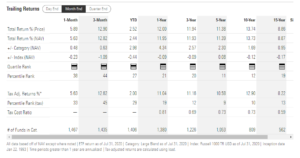

SPY historical return data:

The key metric is the 10-year “average, annual” return for the SPY versus the VWO or the 13% vs 3% return differential.

Emerging markets are out-of-favor as reflected by poor sentiment, and Covid-19 has dealt the asset class a severe blow given that many of these countries do not have the quality health care systems that the US and other developed countries have. VWO and OAKIX represent uncorrelated holdings for the growthier positions in client accounts.

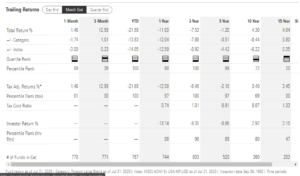

What About Oakmark International ?

As of the end of July, 2020, the Oakmark International was still down 21% and the fund’s percentile rank was still at the wrong end of the extreme, but David Herro was Morningstar’s Portfolio Manager of the Decade from 2000 to 2010, much of it die to China and their annual GDP growth of 15% per year right up until 2008 – 2009, but David Herro is your classic value investor, in what is an out-of-favor asset class, which means that new buys of the fund here likely have less downside – and with patience – more upside, than any time in the last 20 years.

Since the March 23rd lows in the SP 500, the emerging and international markets have improved, with the weaker dollar helping the last few months.

Summary / conclusion: The dollar has bounced sharply the last few days as the greenback hit the lower-end of long trading ranges, but even if it stabilizes here, the weakening of the dollar the last few months should help the asset class. Trying to consider the US election and the impact on the dollar, although much depends on the Congressional composition, a re-elected President should – all other things being equal – likely lead to a stronger dollar, since you would think the President would continue the low-tax, less-regulatory, pro-business agenda. A Biden Presidency, which likely means higher taxes, is a tougher call.

Client’s total allocation between the VWO and the Oakmark International is roughly 8% – 10% of the accounts. The continued dramatic out-performance of the top 5 companies within the SP 500 is likely keeping some allocations away from emerging markets given the performance differential, but if you think about what happened in 1999 and early 2000, when the rotation came, it came quickly.