Part of these negative revisions for 2025 SP 500 EPS growth estimates are undoubtedly from the cautious guidance from Microsoft (lowered revenue guidance for the 2nd quarter in a row), from Alphabet Tuesday night, where cloud growth slowed and then Amazon on Thursday night this past week, where the midpoint of Q1 ’25 revenue guidance was roughly $153 billion versus the $156 billion consensus estimate.

Revenue upside surprise:

- Microsoft: +1%

- Alphabet: 0%

- Amazon: 0%

EPS Upside surprise:

- Microsoft: 0%

- Alphabet: 16%

- Amazon: 25%

It needs a few days to settle and get recorded, but this blog should do a post showing readers EPS and revenue estimate revisions for these companies, to see what damage is done. Apple’s numbers haven’t been updated yet, and neither has Meta while Nvidia doesn’t report for another 2 – 3 weeks.

So here’s how the SP 500 EPS estimates have changed (per the LSEG data) since last week:

- The forward 4-quarter SP 500 EPS estimate fell to $271.24 this week, after last week’s $273.33 and the prior week’s $273.17. This week’s drop in the forward estimate, doesn’t look like much at a $2.09 decline, but that will get some attention.

- The SP 500 PE ratio is 22.2x which hasn’t changed much YTD;

- The SP 500 earnings yield is at 4.50%, still too low in my opinion, and needs to trade up to 5%, which would put the SP 500 earnings yield equivalent to a 20x PE for the benchmark, not out of line with expected ’25 SP 500 EPS growth of 10% – 11% per year;

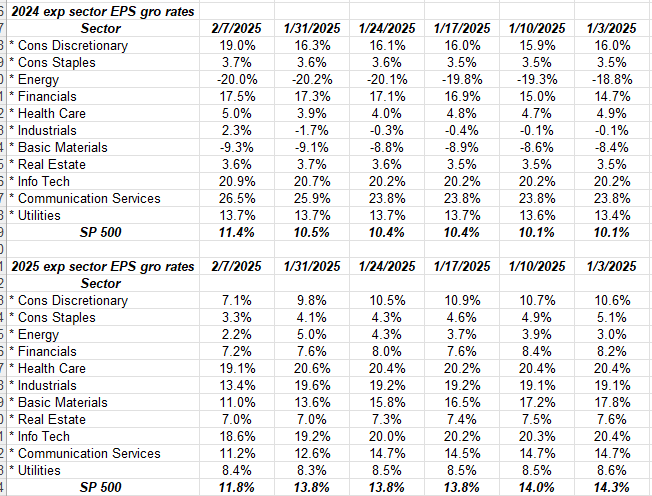

Click to expand on the spreadsheet.

Note the jump in 2024’s expected SP 500 EPS growth for ’24 as Q4 earnings have gotten reported, bit also note how 2025 expected SP 500 EPS growth has been trimmed, somewhat materially.

It was disappointing to see the sharp drop in expected industrial EPS growth, probably somewhat due to Honeywell (HON). 2025 was expected to see a sharp rebound in industrial sector earnings, per the above tables.

Note how the technology sector expected SP EPS growth for full-year 2025, has declined sequentially every week in 2025.

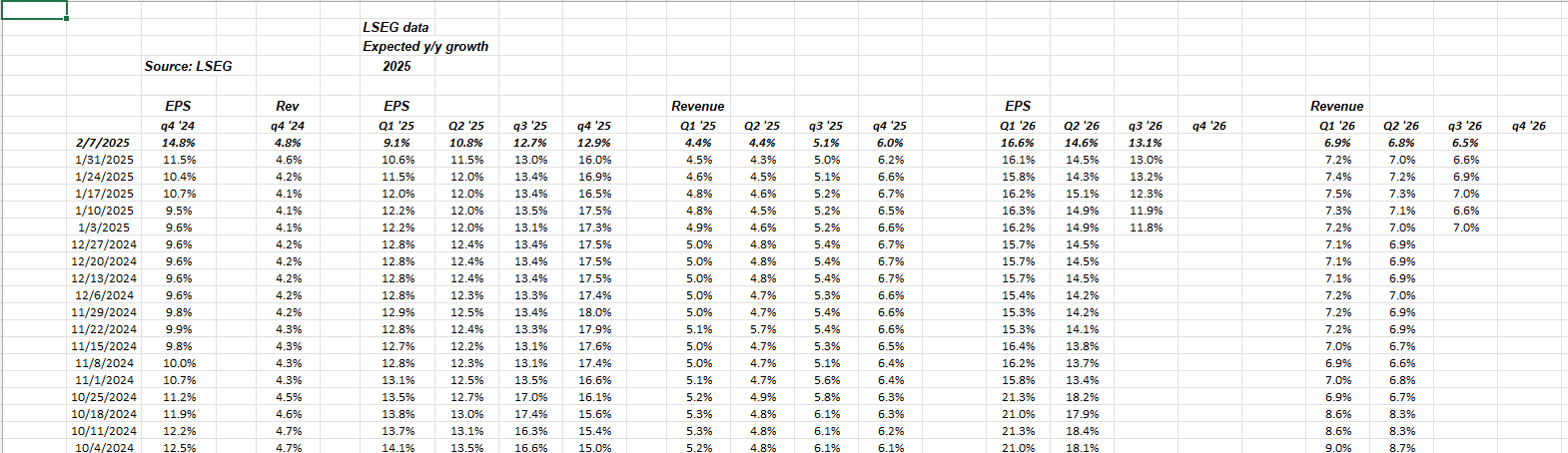

Finally, expand the above spreadsheet and note how Q4 ’24 EPS and revenue growth have grown smartly since Q4 ’24 results started getting released in early January ’25, and then note how the quarterly EPS and revenue expected growth rates have been revised for 2025.

Summary / conclusion: The tough aspect to writing this blog since 2008 and watching SP 500 EPS and revenue data is that the quarterly, annual patterns tend to look the same, until they don’t and the “actual” EPS and revenue data converge from “expected”.

Expected 2025 SP 500 EPS growth is still pretty healthy at 11%, as of this weekend.

The tariff convulsions and the other headlines only make the sector and company analysis more complex.

There is no question there is more uncertainty to the market landscape in 2025, and that should – all other things being equal – result in some PE compression, particularly for the SP 500 and the Nasdaq.

- The Nasdaq Composite peaked at 20,204 on December 16th, ’24 and has not made a new high and ended below it’s 50-day moving average this week;

- The Nasdaq 100 peaked at 539.15 also on December 16th and also has not made a new high since, but has not slipped under it’s 50-day moving average;

- The SP 500 didn’t peak until 6,128.18 on 1/24/25 and hasn’t made a new high since, and also remains above it’s 50-day moving average;

Looking at the 2025 calendar year sector growth rates, the tech sector is still expected to grow almost 2x the SP 500’s expected growth.

This blog post from November ’24 articulated how I was thinking about 2025, but the Fed reducing the fed funds rate further (not that that’s in the cards in the next few months), could change that whole ’25 thought process.

The sentiment in this bull market which is almost 16 years old is nothing like we saw in late ’99, early 2000.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. All data sourced above is from LSEG.

Thanks for reading.

“The sentiment in this bull market which is almost 16 years old is nothing like we saw in late ’99….”

Sorry, you’re suggesting current sentiment is better or worse than that you saw in late ’99?

Best to all,

the late 1990’s were off-the-charts more euphoric, particularly late 1999, early 2000.