Long being fans of Bernie Schaeffer’s technical research and the work produced by Schaeffer’s Investment Research, we noted this chart over the weekend, put out Sunday by Bernie Schaeffer, that is entitled “Chart of the Week” and discusses Bernie’s view of the market, based on this chart: http://myaccount.schaeffersresearch.com/members/services/chartoftheweek/default.aspx?chartid=09790A9A-051C-4244-ADBD-55EBEE917B31. (If readers cannot access Bernie’s chart, the conclusion was that – given YTD action – the SP 500 could be shaping up for a year like 2011, where the SP 500 corrected 20% from the spring high to the October low.

On the other hand, reading Bespoke’s excellent weekly market summary, typically published late Friday afternoon, here is what Bespoke thinks of the market’s expected direction for the rest of 2015, given the first 13 weeks of the year:

1.) The range between the highest and lowest prices for the SP 500 this year is 6.27%, so equity volatility is very low (my conclusion, not Bespoke’s).

2.) Per the Bespoke data, “in the 9 years where we’ve gone completely sideways through early May, the index has been higher over the remainder of the year 8 times, for an average gain of 4.76%.”

Two completely opposite stock market predictions, based on the same market action.

So what would be the difference in 2011 vs. 2015 ? My guess is interest rates.

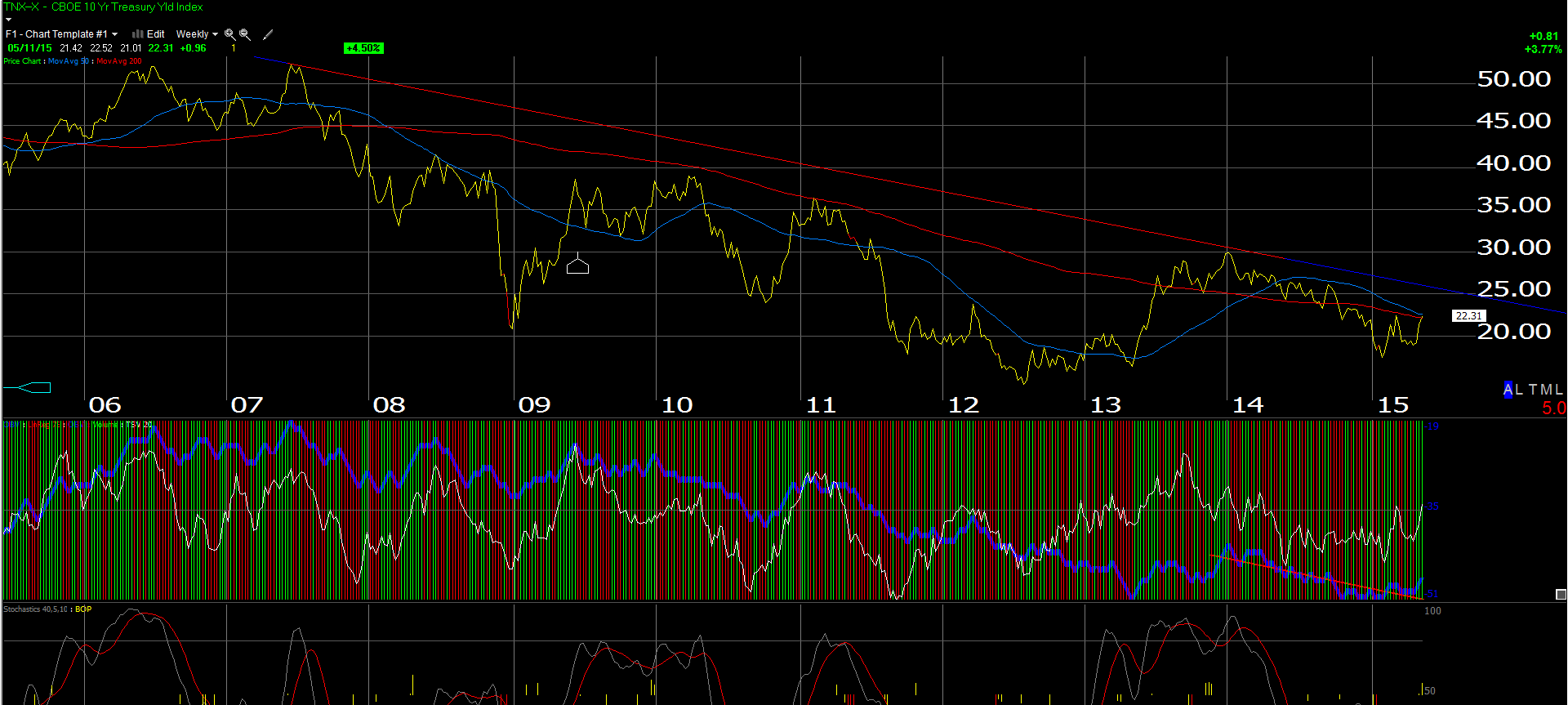

This is a weekly chart of the TNX or the CBOE 10-year Treasury yield contract.

A trade in yield above 2.25% and I think we see 2.50% quickly. A trade through 2.50% and we would trade above the downtrend line off the 2007 high yield over 5%, that wasn’t penetrated even in late 2013. Note where the “yield rally” stopped in 2013 i.e. right at the downtrend line.

The two stocks that would be sensitive to changes in interest rates or benefit from higher interest rates, both financial names, are Chicago Merc (CME) and Charles Schwab (SCHW).

Here is one final anecdotal point: a former portfolio manager I worked with in a prior life, and a guy I have high regard for personally and professionally, who currently manages about $2 billion in fixed income for an under-the-radar Chicago firm, responded to an email I had sent him bemoaning the fact that it appears that Treasuries are the only asset class immune to the “reversion to the mean” trade. His response – “we’ve been here before” – meaning we’ve seen back up in rates and they were temporary. That is definitely not a criticism, but it speaks to the complacency I see around interest rates and Treasuries.

The 10-year Treasury yield is trading above 2.25% as we speak.

Through 2.50% on the 10-year Treasury yield and I think it really will be “different this time”.