One of our favorite retailers has gotten pretty beaten up of late, after WFM guided lower in their November ’13 quarterly earnings release. With their q4 ’13 release last November, WFM printed 2% revenue growth, the lowest rate of revenue growth since 2009, and just 9% operating income growth and 7% EPS growth, also the lowest since 2009.

Comp guidance was 5.5% – 7% for 2014, which is below the 7.5% to 9% WFM had been seeing the last few years.

Part of the problem last quarter was Boston cannibalization, with WFM’s close competitor, Johnnie’s Foodmaster, cutting into WFM comp’s by 30 bp’s last quarter. However I’m not convinced the problem is entirely Boston-related: as a huge Whole Foods fan here in Chicago, living in the tony area of Lincoln Park, there are now at least 3 (!) new WFM competitors in the last year, squeezing Whole Food’s business: Mariano’s ( a division of Roundy’s founded by Bob Mariano, who left Dominick’s to run a better grocery shop), Mrs. Green’s, and Plum Market, a small Detroit operation that leaves Plum Market looking and feeling exactly like WFM). In addition, we still have the old stand-by’s like Trader Joe’s, Treasure Island, etc. etc.

Now the good part of what is happening on Chicago is that the old Dominick’s and Jewel’s are closing down and newer, fresher competitors like WFM are filling the gap, particularly in some of the rougher parts of Chicago.

The positive part of WFM’s story is that management’s new store goal is 1,000 stores in the US, versus their 362 stores currently, meaning that WFM is supposedly just 1/3rd of the way through their secular build out. The problem being is that if WFM is making that info available as a way to identify the market opportunity for investors, then that is what is likely driving the sudden expansion of WFM competitors. WFM’s competition is seeing the same market opportunity as WFM is, apparently.

There is nothing really cheap about the stock currently with 2014 and 2015 EPS estimates currently at $1.68 and $1.98 for expected growth this year and next of 15% and 18%. Fiscal 2013 grew at 17%. Revenue growth is still projected to grow at 13% in 2014 and ’15, after growing 10% in 2013.

In addition, after growing revenue +20% for most years from 2000 – 2008, the post Great Recession revenue growth has been mid-teens, and I wonder if WFM is entering a new slower, steadier, growth phase.

What I am a little worried about is that slight downward pressure continues the ’14 and ’15 EPS and revenue estimates. The retail climate hasn’t been that great of late, as general merchandising retailers have come under pressure and retail stocks have traded heavy.

Whole Foods (like Starbuck’s) is one of those secular growth stories that never get truly cheap, and an investor only gets low-risk buying opportunities when the stock gets oversold as it is today.

We added to WFM today, with a mind to sell some near the old breakdown gap in the low $60’s. Do I worry about ? Sure. Could the iconic specialty grocer be attracting a ton of competition ? Sure.

Here is Gary Morrow’s excellent technical take on WFM: for us a trade on heavy volume below $50, wouldn’t be welcome, but the stock looks to be setting up for a decent bounce.

Whole Foods Struggles to Find its Footing

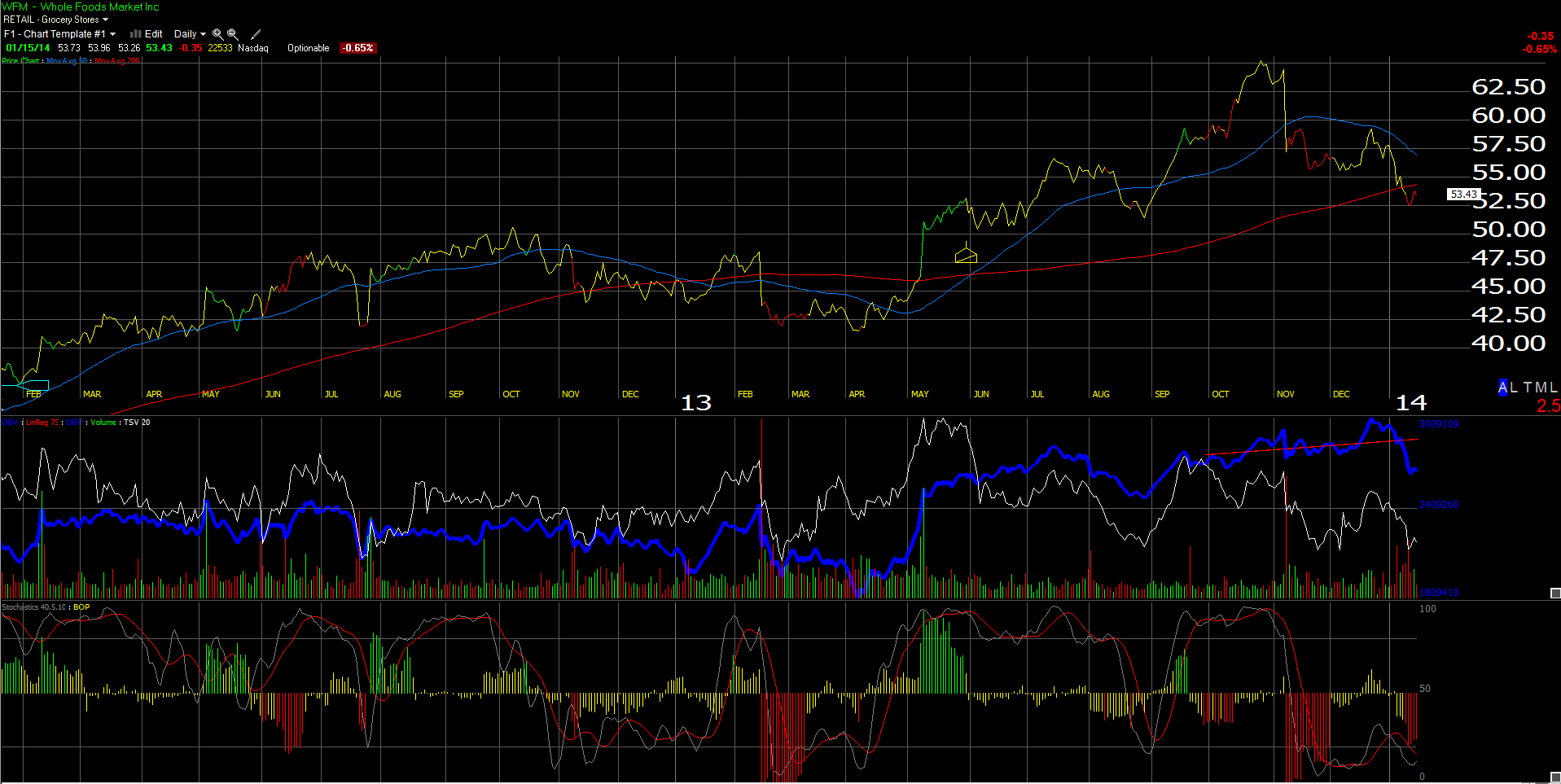

Whole Foods has struggled since its massive November 7th breakdown. A disappointing quarterly report lead to a huge gap lower open. WFM dropped over 10% on the news while volume jumped to its heaviest level in nine months. This huge shift in momentum was a sharp reversal from the impressive bullish action that dominated the the previous ten weeks.

WFM was unable to recover much of the news inspired collapse. The stock bounced up to the $59.50 area in the immediate aftermath but sold off again later in the month. WFM rallied again in mid December after reaching an oversold reading but the rebound was stopped dead in its tracks near $59.50. The sell off from this double top was even more severe, especially this month as volume began to pick up. Last week the stock fell below its supportive 200 day moving average for the first time since May. With this key level now overhead, WFM may require and extended base before a healthy rebound can take place.

Whole Foods is trading just above a major support zone. Following the huge May 8th breakout the stock held the $50.00 to $51.00 area at its June, July and August lows. This zone also includes the stock’s 2012 peak of $50.90. If the stock can hold in this area in the coming weeks a solid base could be built. Easing volume and a divergent oversold reading would bolster the pattern. In addition WFM would be approximately 20% below its 2013 high set just eleven weeks ago. A recovery rally would have significant potential.

We still believe in the secular growth story, albeit a little more nervously.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager