The 60% /40% balanced portfolio (SP 500 / Batclays Aggregate) had returned -12.37% YTD as of Friday, August 26th’s close. The balanced portfolio has lost roughly 300 bp’s in return since the post June ’22 low rally peaked two weeks ago with the week ended August 12, 2022.

Rarely do I write on economic data strictly since the data is reported with a substantial lag (except jobless claims and some of the PMI’s) and there are so many other sources of solid economic analysis and review. My long-time favorite, who I’ve followed since the late 1980’s and his days at Harris Bank in Chicago, is Brian Wesbury, now of First Trust.

However, after Powell’s Jackson Hole speech on Friday, August 26th, 2022, and the stock market reaction to the speech, (and after reading the actual speech itself rather than the financial media’s interpretation of the speech), my takeaway was that Jay Powell, the Fed and the FOMC are now focusing on wage inflation or the “labor” component, rather than simply “price” or goods and services inflation. (Again, please understand, this is my own take from the speech and it could just as easily be very wrong as it is right.)

The July ’22 payroll report was way above expectations at 528,000 “net new jobs” created, with 471,000 new new jobs created from the private sector. I don’t think it’s an exaggeration when I say that number turned a lot of heads and got a lot of people’s attention when it was released. That print was 2x what was expected for July ’22’s payroll growth and a lot of the Street was expecting slower growth and a higher unemployment rate.

In addition average hourly earnings (AHE) print for the July ’22 report was +0.5%, versus the +0.3% expected.

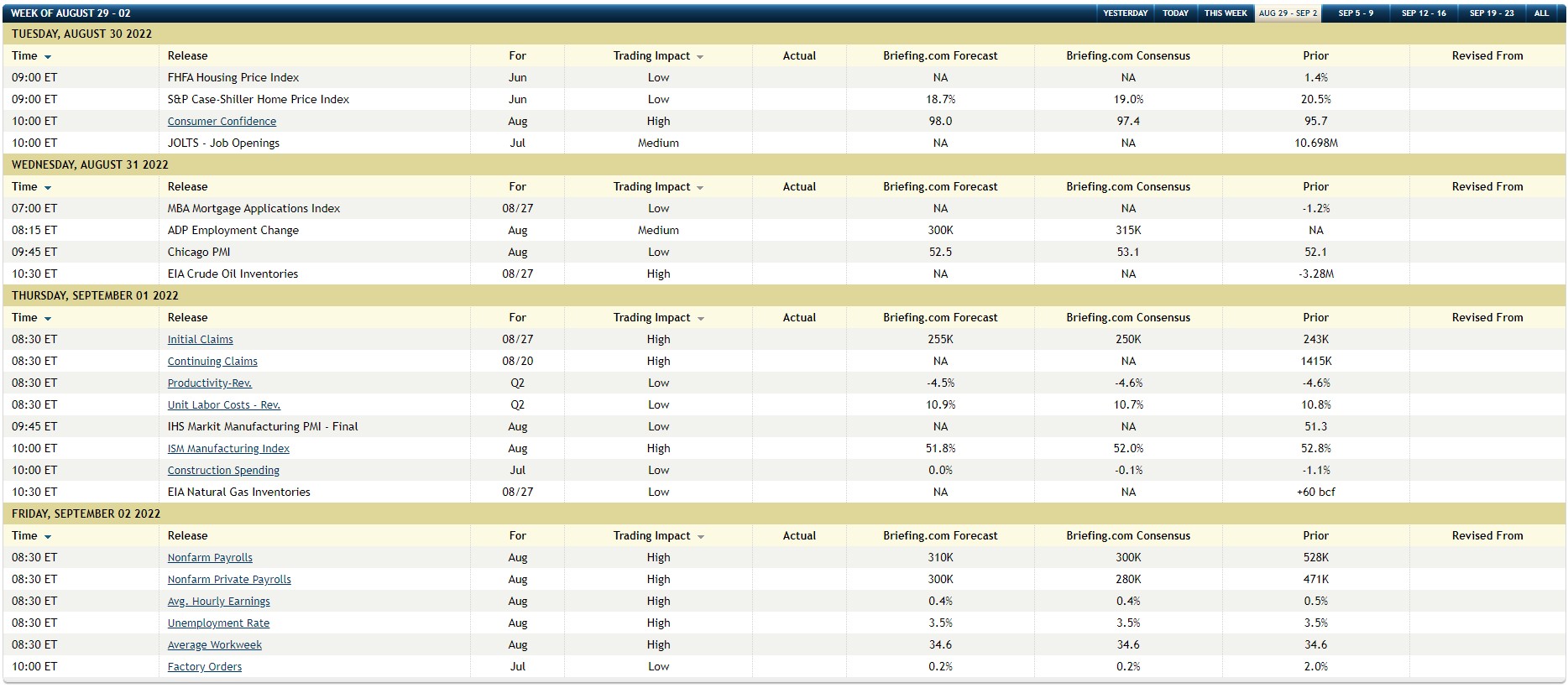

Here’s what the Street is looking for this week on the economic release front and more specifically, August, 2022’s jobs report due out on Friday September 2, 2022:

Any number north of 500,000 for total net new jobs created and an AHE at +0.5% or better would likely not be well received, and would likely guarantee another 75 bp move (or maybe more) at the September ’22 FOMC meeting.

A number inline with Briefing.com’s consensus at 300,000 or so and an AHE of +0.4%, still doesn’t move the FOMC off the current path.

It’s one opinion, but I think you need a 200,000’ish August ’22 payroll report and an AHE at +0.3% or better to generate a rally in the 2-year Treasury, rather than the persistent, steady increase in the 2-year Treasury yield we’ve been seeing.

The weekly jobless claims and continuing claims have stopped weakening, which could actually portend a somewhat stronger-than-expected report come this Friday, September 2nd, 2022.

Summary / conclusion: Price inflation is clearly expected to moderate in the coming months with Treasury break-evens expecting 2.5% inflation rate over the next 10 years, the price of crude oil and gasoline falling and even used car prices have started to rollover (per the weekly Bespoke Report), but the labor market has clearly been strong and wages are clearly not weakening, which makes sense if you watch the JOLTS (job opening and labor turnover survey) report.

This is the last shoe to fall for the Fed. Personally, I’m not expecting much of a weakening with the August payroll report, but would think the September ’22 report (due for release in early October ’22) would start to show some softening.

That is strictly a guess too, but various “price” indices have been softening for the last few months.

The stock market’s reaction to the better-than-expected PCE data on Friday morning, August 26th, and even the GDP deflator from Thursday’s GDP release was better news for monetary policy. I’ve never seen the data personally, but with a US economy bumping along at a 1% – 1.5% GDP growth rate, I’ve wondered what that would means from a monthly job growth extrapolation perspective. You’d think a US economy growing at 1% – 1.5% can’t sustain monthly job creation of 525,000. One of the two data points has to reflect reality.

Anyway, take all of this with substantial skepticism and a serious grain of salt. It’s just an opinion, but expect “price” inflation to continue toe moderate, but the thorn in the Fed’s side today is wage inflation and the labor market.

Thanks for reading.