Looking at the capital markets action this week, credit spreads improved, the US dollar fell (as measured by the UUP), the 10-year and 30-year Treasury yields haven’t made new highs in weeks, the PCE deflator data came in as expected, and lower year-over-year, and stocks bounced sharply.

This week’s returns:

- UUP: -1.38%

- HYG: +4.81%

- JNK: +4.87%

- AGG: +0.94%

- SPY: +6.59%

- Nasdaq Comp: +6.8%

- QQQ: +7.07%

You could call this week just a huge reversal of the 7 – 8 week trends.

The SP 500, Nasdaq Composite and the Nasdaq 100 remain very oversold, which is a plus.

The SP 500’s bounce off 3,800 last Friday was a significant move: as this blog pointed out a number of times, the 3,800 level on the SP 500 was a 1/3rd retracement of the March ’20 lows to the early January ’22 highs, which is (symmetrically, anyway) a perfect pullback or correction that doesn’t have to indicate a secular bear market is at hand.

SP 500 data:

- The forward 4-quarter estimate fell to $233.49 from last week’s $235.22. The last 5 – 6 weeks has seen the forward estimate gyrate between $234 – $235 until this week;

- The PE ratio on the forward estimate rose to 17.7x from last week’s 16.5x based on the 6.2% increase in the SP 500 this week;

- The SP 500 earnings yield fell to 5.62% from 6.03% last week;

- The Q1 ’22 bottom-up estimate for the SP 500 rose a penny to $54.85 from $54.84 last week;

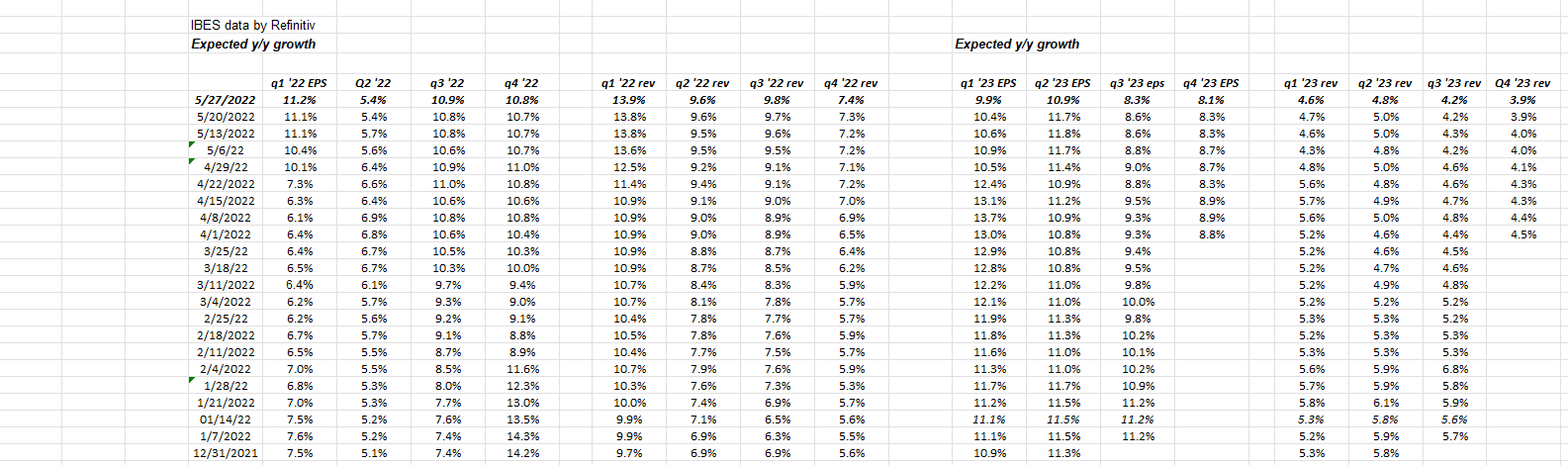

Watching expected quarterly EPS and revenue growth rates:

Note the slippage in all the 2023 quarterly growth rates, for both SP 500 EPS and revenue. These tend to jump around, but the ’23 EPS cuts stood out.

Of the last 7 weeks for the forward 4-quarter estimate, 4 weeks showed sequential declines. The forward estimate tonight of $233.49 is almost exactly where it was on April 15th, 2022.

It’s clear the sell-side is starting to become (at least) a bit more cautious as Q1 ’22 earnings season ends, and those companies reporting a May quarter will soon start to report.

Summary / conclusion: The Treasury market hasn’t seen higher yields on the 10-year and 30-year for several weeks. Whether inflation rolling over, or worries over a recession starting, there is some tempering of the harsh “stagflation” argument beginning.

The jobs report next Friday, June 3, 2022, will probably reflect another 300k – 400k quarter of “net new jobs added” for the US economy.

There has been such a convoluted series of events happen over the last two years, including Ukraine, it’s hard to sort out the market implications for the various moving parts. Let’s sort out the variables:

- Lower inflation – definite plus for stocks and bonds. This morning’s PCE deflator was a start. Most aren’t on board the “disinflation” theme;

- Job growth: job losses are great for bonds, bad for stocks. Slower job growth and the potential for wage growth slowing a definite plus, more so for stocks and bonds;

- Falling dollar: a definite plus particularly for non-US;

- Economic data: it seemed to me with the stock market the last 3 weeks, worries over the US slipping into a recession seemed to increase markedly.

Remember, for those of who were around in 1994, the FOMC and Greenspan raised rates 6 times, and the total return for 1994 for the SP 500 was +1%. 1995 was a monster rally in the SP 500 and that was 13 years into that secular bull market.

Of everything that bounced this week, the high-yield returns were most encouraging. Spreads were widening probably due to duration as much as credit concerns.

It’s all a guess. Take everything here with a grain of salt. None of this is a recommendation or advice.

Thanks for reading.