A couple interesting metrics jumped out on the SP 500 EPS spreadsheet this week:

- The SP 500 EPS estimate has risen from $223 to $225 in the first 6 – 7 weeks of 2022;

- The PE has fallen from 21x in early January ’22 to 19x as of February 18, 2022;

- The SP 500 earnings yield has now hit a high of 5.18%, the highest since March – April, 2020.

Here’s a rundown of the metrics provided each week:

- The forward 4-quarter EPS came in this week at $225,41, up from $225.15 last week and the year’s start of $223;

- The PE ratio this week ended at 19.2x after the weekly loss for the SP 500 of -1.50%

- The SP 500 earnings yield jumped to 5.18% versus 5.09% last week;

In March, 2020, the SP 500 earnings yield rose to 6.5%, and then again in December ’18 it rose to 7%. This week’s 5.18% doesn’t sound like much, but it’s relatively high for the last 2 years.

5 of the 7 weeks to start 2022 have seen the SP 500 end the week with a negative return.

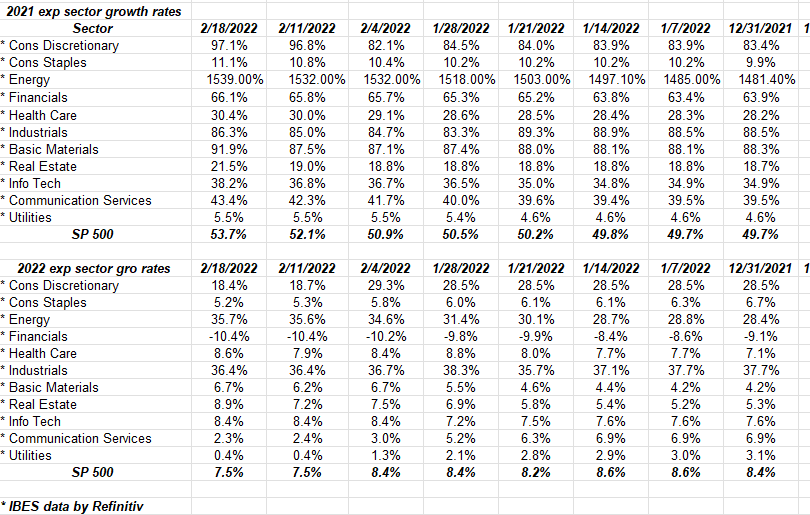

This table from IBES by Refinitiv shows how the SP 500 sectors are expected to look in terms of EPS growth in 2022 versus 2021.

The village idiots out there most of whom don’t even follow SP 500 earnings are using the expected 7% – 8% EPS growth rate for 2022 as a reason to be bearish, while 2022 is really all about tougher comp’s against 2021, particularly for technology and financial sectors.

Energy investors will face tougher comp’s as 2022 progresses.

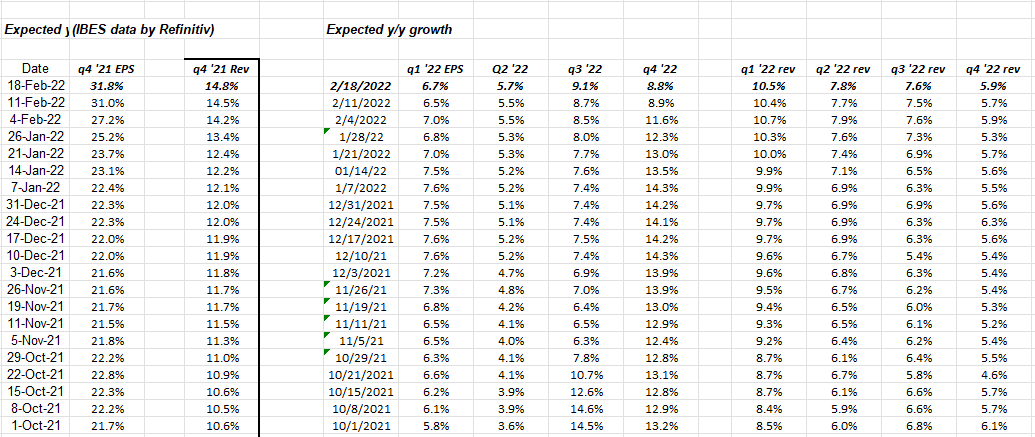

This table which uses IBES data by Refinitiv but is proprietary creation, shows that Q4 ’21 will end very strong.

However note the revenue growth for 2022 by quarter: the strongest “expected” rate of revenue growth will be Q1 ’22 and then it will gradually decline into Q4 ’22.

Don’t take this as gospel though: analyst estimates since the pandemic started have been exceptionally conservative and every quarter since Q1 ’20 has seen very strong upside surprises.

Im expecting 2022 will be relatively “normal” year earnings-wise.

Summary / conclusion: With Q4 ’21 earnings reporting season unofficially ending this week with Walmart’s release (and both Walmart and Cisco – two 1990’s growth giants – saw strong reports and higher stocks following their earnings release) investors will look at March ’22 earnings releases which will have a February ’22 end dat for their reporting periods. In other words, we start to see what early ’22 looks like for a number of companies.

Ukraine is a complete wild card, but I expect Q1 ’22 will be another decent quarter of large-cap earnings. The above spreadsheet is still expecting 10% revenue growth for Q1 ’22 and that’s been constant the last 5 – 6 weeks when the overall SP 500 has been pretty weak in terms of price action.

The interest rate outlook can influence stock and bond valuations, but not necessarily company operations depending on it’s capital structure, etc.

The SP 500 earnings yield got my attention this week.

None of this is advice and take it all with substantial skepticism. Ukraine can change the markets quickly, and it may be entirely discounted already.

Thanks for reading.