Every quarter, JP Morgan’s Dr. David Kelly and the JP Morgan Research team publish their “Guide to the Market”, which is a 70 – 75 page look at the capital markets, the economy, Fed policy, the dollar and any other important aspect to the investment and financial world.

Using the SP 500’s valuation metrics today, found on page 5 of this quarter’s Guide, this blog has tracked the metrics over time, rather than looking at a single snapshot every quarter.

The forward PE and the Price-to-Cash-Flow metrics are nearing 2 standard deviations above normal (the price to cash-flow is actually above 2 standard deviations), perhaps not unexpected given the 31% decline in 2nd quarter ’20 GDP.

The SP 500’s dividend yield is at its lowest yield since late 2015.

I guess the eternal question is, “Will price likely move down or SP 500 earnings, cash-flow and other metrics move up to bring the valuation metrics back in line ?”

We should probably assume some combination of both will occur.

SP 500 Earnings Update:

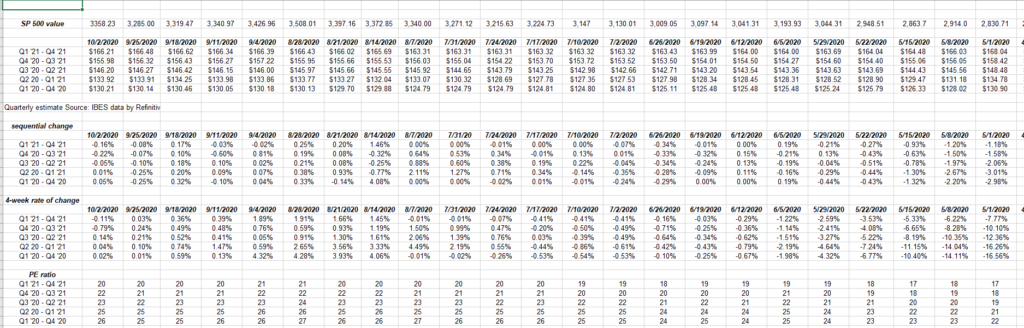

The quarterly bump occurred in the IBES data by Refinitiv, thus putting the “forward 4-quarter estimate” at $155.98, this Friday, October 2nd, versus last week’s $146.27.

The PE on the forward estimate is back to a reasonable 21.5x (also supported by the first spreadsheet using JP Morgan’s “Guide” data).

The “average PE” for calendar 2020 and 2021 is 23x today.

The “average” expected SP 500 EPS growth for calendar 2020 and 2021 is still 4%.

The SP 500 earnings yield has jumped to 4.64%, versus last week’s 4.35%, or the highest earnings yield since early May ’20.

The pullback in the SP 500 and the Nasdaq is in fact helping the SP earnings yield work it’s way higher as forward earnings continue to improve.

SP 500 Forward Earning Curve

Until bank earnings start being reported the week of October 12th, we should expect some softness in SP 500 earnings as – absence any news – sell-side analysts tend to get nervous and tweek numbers lower. Better to miss an upside surprise than a downside mess, seems to be preferred risk – reward over the years.

Summary / Conclusion: So many consider today’s market “overvalued” yet there is always the question, will price move lower or the valuation metrics move higher to correct the valuation issue. It’s the never-ending debate and discussion that ultimately leads nowhere in my opinion.

More and more it’s the level of interest rates that worries me, but given the current state of affairs there won’t likely be any change in monetary policy for some time.

Thanks for reading. Will likely write on other topics this weekend.